In personal or family retirement planning, several key factors should be considered comprehensively, including: retirement goals and lifestyle (expected retirement age, estimated living expenses, and income needs during retirement), retirement asset accumulation (such as 401(k), IRA, Roth accounts, investment accounts, pensions, etc.), lifetime income sources (such as Social Security benefits, pensions, and annuities to ensure a stable cash flow throughout retirement), investment and risk management (adjusting asset allocation according to different stages of retirement while balancing growth and principal protection), tax planning (strategically coordinating withdrawals from pre-tax, after-tax, and tax-free accounts to minimize taxes during retirement), healthcare and long-term care planning (including Medicare, long-term care expenses, and healthcare risks), inflation protection (ensuring that assets and retirement income keep pace with rising living costs), estate and wealth transfer planning (protecting family wealth through insurance, trusts, beneficiary designations, and other estate planning strategies), as well as emergency reserves and liquidity management (maintaining sufficient cash reserves to cover unexpected expenses).

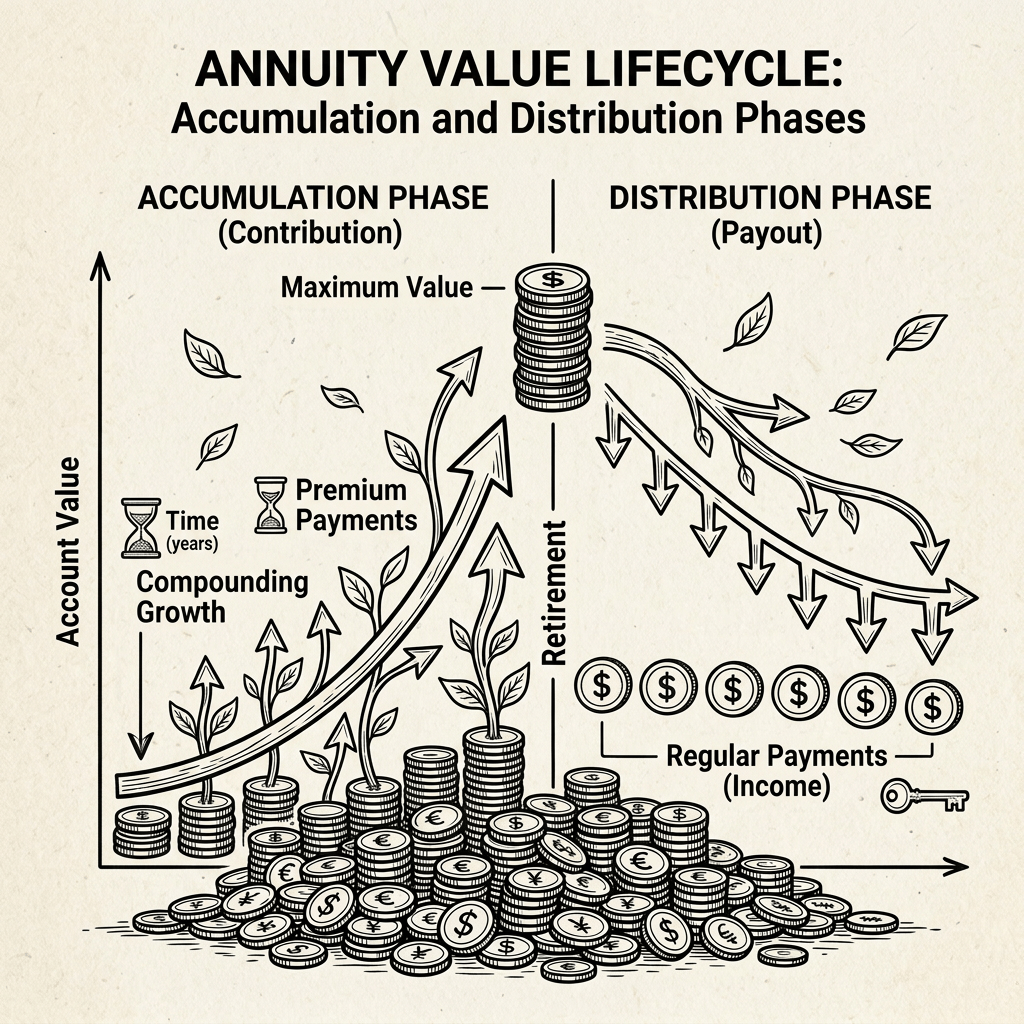

Among the various sources of lifetime retirement income, annuities serve as an important supplemental income source. Many people believe that annuities should only be purchased after retirement. In reality, the optimal time to purchase an annuity is often many years before income distributions begin. Therefore, early annuity planning is essential to achieving long-term retirement goals, including stable lifetime income, tax efficiency, effective risk management, and/or an orderly transfer of wealth.

I. When Is the Best Time to Purchase an Annuity?

The answer depends on your financial objectives.

Stage One: Ages 30–45 (Generally Not the Ideal Time, with Some Exceptions)

In general, younger individuals are not encouraged to allocate a significant portion of their assets to annuities because:

- They still have 20–30 or more years to invest.

- Asset growth should be the primary objective.

- Liquidity is generally more important.

- Index funds, 401(k) plans, IRAs, and similar investment vehicles are usually more appropriate.

Exceptions:

- Individuals with high incomes who have already maximized contributions to their 401(k) and IRA accounts and wish to continue enjoying tax-deferred growth.

- Individuals who wish to lock in future retirement income at an early stage.

Stage Two: Ages 45–60 (When Many People Begin Annuity Planning)

This is the age range during which many financial professionals recommend considering annuities.

Reasons include:

- Retirement is approximately 10–20 years away.

- Financial priorities begin shifting from wealth accumulation to wealth preservation.

- The potential impact of a major stock market downturn becomes increasingly significant.

- There is still sufficient time to benefit from compound growth over the next 10 years or more.

Example:

At age 45:

- Invest $100,000

- Allow it to grow for 15–20 years

- Begin receiving retirement income at ages 60–65

At this stage, compound growth can still produce meaningful long-term results.

Stage Three: Ages 55–70 (The Most Common Period for Purchasing Annuities)

This is the age group in which the majority of annuities are purchased in the United States.

Many people during this stage experience events such as:

- Retirement

- Selling a home

- Receiving an inheritance

- Rolling over a 401(k)

- Receiving a lump-sum pension distribution (Pension Lump Sum)

Their primary goals often include:

- Principal protection

- Guaranteed lifetime income

- Protection against market downturns

- Leaving a financial legacy

As a result, substantial assets are commonly allocated to:

- Fixed Annuities

- Fixed Indexed Annuities (FIAs)

- Income Annuities

Stage Four: After Age 70 (Annuities Can Still Be Purchased)

The primary objectives at this stage include:

- Beginning retirement income immediately

- Long-term care planning

- Estate planning

- Reducing investment management responsibilities

However, as individuals grow older, the available time for long-term accumulation becomes shorter. Therefore, many people choose to complete their annuity allocation around age 60.

II. What Sources of Funds Can Be Used to Purchase Annuities?

In the U.S. market, funds used to purchase annuities generally fall into two primary categories.

1. Qualified Money (Retirement Account Assets)

These funds originate from qualified retirement accounts, such as:

- 401(k)

- 403(b)

- 457(b)

- Traditional IRA

- SEP IRA

- SIMPLE IRA

- Pension Rollovers

These assets can generally be rolled directly into an annuity within a qualified retirement account.

Advantages:

- Continue tax-deferred growth

- No current-year income tax upon rollover

- Taxes are generally deferred until distributions are taken

Example:

At retirement:

401(k)

↓

Roll over to an IRA

↓

Purchase a Fixed Indexed Annuity (FIA) within the IRA

↓

Receive retirement income during retirement.

2. Non-Qualified Money (After-Tax Funds)

These funds may include:

- Cash savings in bank accounts

- Matured Certificates of Deposit (CDs)

- Proceeds from selling stocks

- Proceeds from selling mutual funds

- Cash from the sale of a home

- Inheritance proceeds

- Business sale proceeds

- Savings account balances

Characteristics:

These funds have already been subject to income tax.

Therefore, when distributions are taken later, only the earnings portion is generally taxable, while the original principal is not taxed again.

This approach is commonly used by many high-net-worth families.

III. What Other Types of Funds Can Be Used?

Examples include:

- Inherited IRA assets (subject to applicable distribution rules)

- Trust assets

- Corporate funds (for certain business purposes)

- Legal settlements

- Retirement bonuses

- Deferred Compensation plans

IV. What Are the Main Types of Annuities in the United States?

Based on how they generate growth, annuities offered by U.S. insurance companies generally fall into the following categories.

① Fixed Annuity

Key Features:

- Fixed interest rate

- Principal protection

- Interest rate is determined in advance

Suitable For:

- Conservative investors with low risk tolerance

- Short-term cash allocation

- Periods of relatively high interest rates

② Fixed Indexed Annuity (FIA)

This has been one of the fastest-growing annuity categories in recent years.

Key Features:

- Principal protection (subject to the product’s guarantee provisions)

- Earnings are linked to the performance of a market index (such as the S&P 500)

- Opportunity to participate in market gains

- Principal generally will not decline due to negative index performance (subject to the terms and conditions of the contract)

Many products also offer optional features such as:

- Income Rider (provides guaranteed lifetime income)

- LTC Rider (provides long-term care benefits)

- Death Benefit (provides benefits to beneficiaries upon the owner’s death)

FIAs are an excellent retirement planning solution for many individuals and families.

③ Variable Annuity (VA)

Key Features:

The account value is invested in:

- Stock funds

- Bond funds

- Balanced funds

Advantages:

- High growth potential.

Disadvantages:

- Principal is subject to market risk and may decline.

- Fees are generally higher than those of other annuity products.

④ Registered Index-Linked Annuity (RILA)

RILAs have experienced rapid growth in recent years.

Characteristics:

They fall somewhere between:

- Fixed Indexed Annuities (FIAs)

- Variable Annuities (VAs)

They offer:

- Limited downside protection

- Greater upside growth potential

Suitable For:

Individuals who are willing to accept a moderate level of market risk in exchange for greater growth potential.

In addition, annuities may also be classified according to their primary purpose: Income Annuities and Growth Annuities.

Income Annuity

An Income Annuity is designed primarily to provide a stable and sustainable stream of retirement income. After contributing a lump sum, the contract owner may begin receiving payments immediately or defer payments until a future date. Income may be distributed monthly, quarterly, or annually, and may continue for a fixed period or for life. Income annuities help reduce the risk of outliving one’s retirement savings and serve as an important component of a comprehensive retirement income strategy.

Growth Annuity

A Growth Annuity is designed primarily for long-term asset accumulation and tax-deferred growth. During the accumulation phase, the contract value grows through fixed interest, index-linked crediting strategies, or market-based investments, depending on the type of annuity. Income is typically deferred until retirement, at which point the accumulated value can be converted into guaranteed lifetime income or withdrawn as needed. The primary objective is to help investors grow their assets while managing risk, thereby building greater financial security for retirement.

V. Recommended Annuity Types Based on Financial Objectives

| Financial Goal | Recommended Annuity Type |

| Principal protection | Fixed Annuity |

| Principal protection with higher growth potential | Fixed Indexed Annuity (FIA) |

| Maximum growth potential | Variable Annuity |

| Guaranteed lifetime income | Immediate Income Annuity / Deferred Income Annuity |

| Willing to accept moderate risk for greater upside potential | Registered Index-Linked Annuity (RILA) |

VI. Recommendations for Most Individuals and Families

For middle-income families between the ages of 45 and 65, a common retirement planning strategy includes:

- Continue building retirement assets through qualified retirement accounts such as 401(k)s and IRAs.

- Approximately 10–15 years before retirement, consider allocating a portion of retirement assets or after-tax savings to a Fixed Indexed Annuity (FIA) to reduce exposure to market volatility while establishing a reliable source of future lifetime income.

Therefore, when developing a comprehensive family financial plan, beginning annuity planning between ages 45 and 60 and starting retirement income between ages 60 and 70 is generally considered a reasonable time frame. However, the optimal strategy should always be tailored to each individual’s circumstances, including the desired retirement age, Social Security claiming strategy, other retirement assets, and future cash flow needs.

Leave a comment