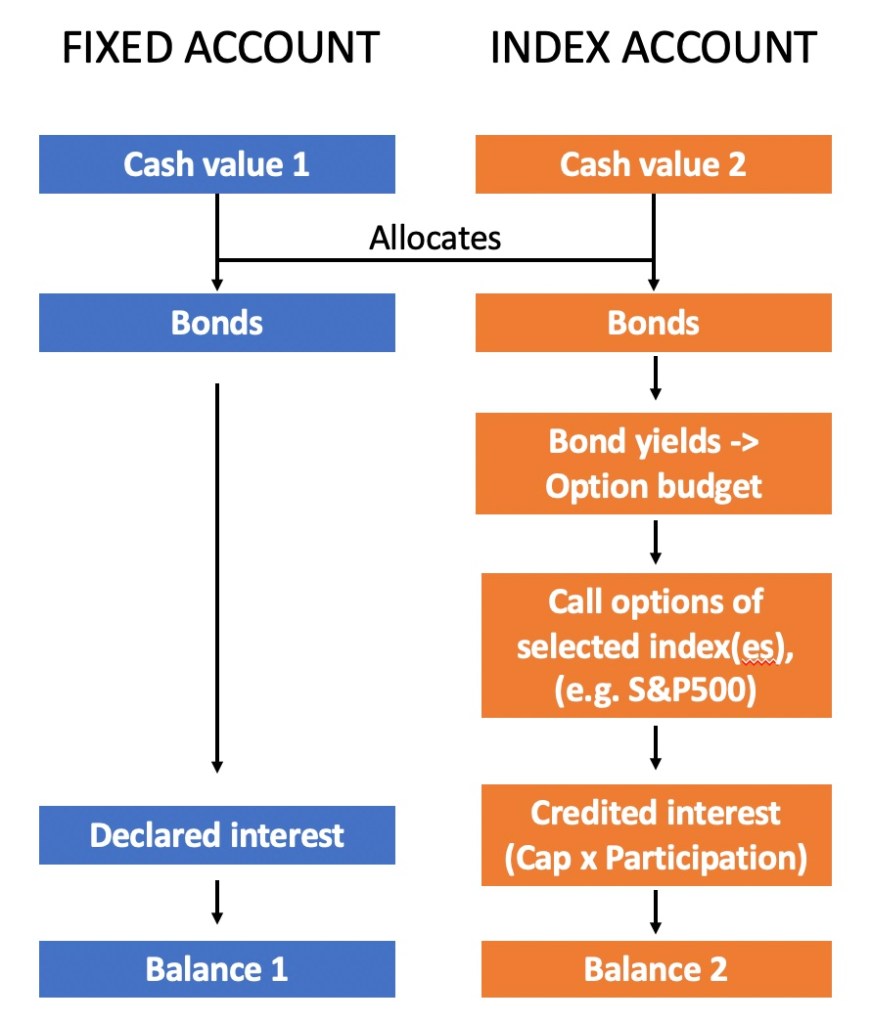

In an Indexed Universal Life (IUL) policy, there are two types of accounts: the Fixed Account and the Index Account. The policy owner can allocate the cash value between these two accounts at the start of each ‘index segment’ period (typically one year). In this section, I will focus on explaining how these accounts work and what happens when the cash value is divided between them, using a simplified illustration.

Part 1: Working Mechanisms

1. Fixed Account mechanics

- The Fixed Account is declared-rate interest, similar to a general account annuity.

- The insurer invests those assets mainly in high-grade bonds and declares an annual interest rate (subject to a guaranteed minimum, usually 2–3%).

- Since the credited rate is not tied to an index, no options are needed.

2. Index Account mechanics

- When the policy owner allocates to an Index Account, the insurer must translate bond yields into potential index-linked credits.

- To do that, they use the options budget (bond yield – margin) to buy call options on the chosen index.

- Options provide the upside potential (subject to cap/participation) while preserving the 0% crediting floor.

3. Policy owner’s control (see Figure 1 below)

- By selecting Fixed Account only, the policy owner is essentially choosing a “conservative” path — stable, declared returns, no market-linked upside.

- By selecting Index Accounts, or allocating all or a portion of cash value to Index Account, the policy owner is choosing to participate in equity-linked credits, which require the insurer to engage in options trading.

⚖️ Trade-off for policy owner

- Fixed Account = stable, predictable, but usually lower crediting rate (e.g., 3–5%).

- Index Accounts = higher upside potential, downside floor at 0%, but subject to caps, pars, and insurer option pricing.

Figure 1: Two accounts in IUL

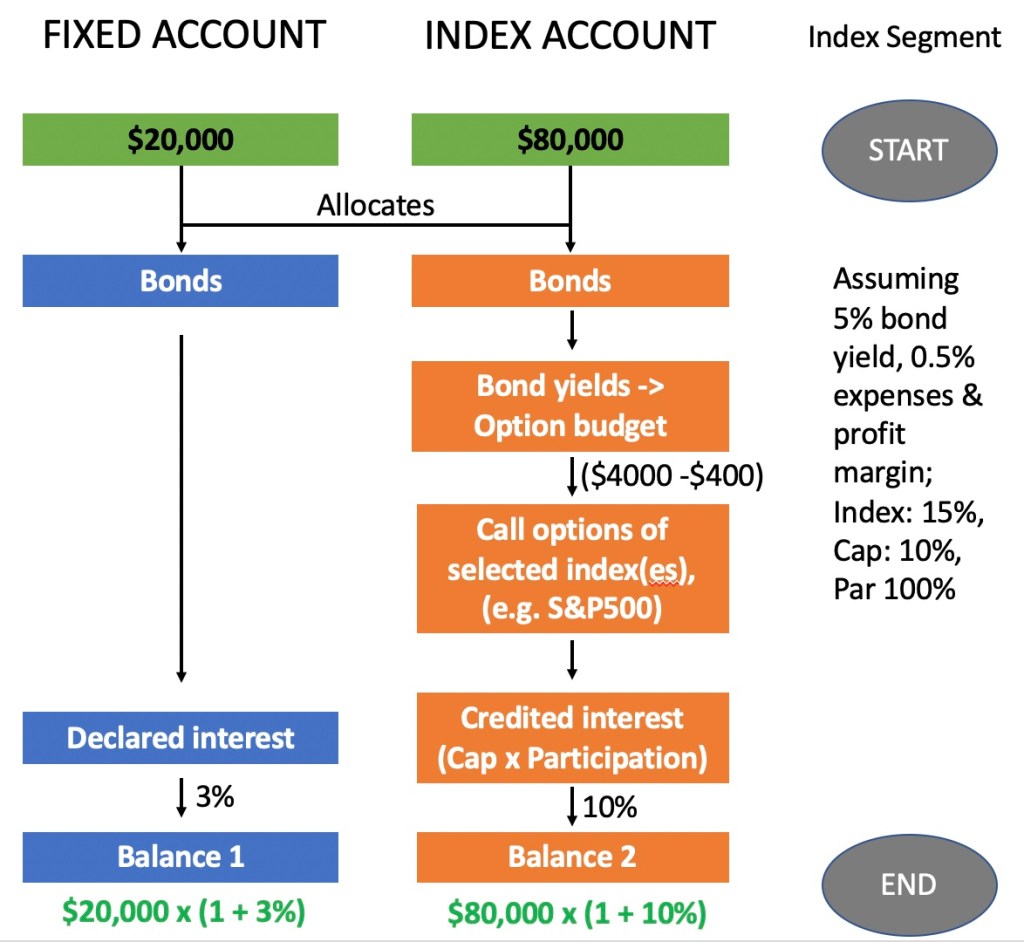

Part 2: Simplified illustration

Given total cash value after the charges and fees is $100,000 with $20,000 going to Fixed Account and $80,000 to Index Account (linked to chosen index, e.g. S&P500).

1) Fixed Account Portion – $20,000

- This money stays in the insurer’s general account, mainly invested in bonds.

- The insurer uses it to generate a stable bond yield (e.g., 4–5% depending on market rates).

- From that yield, the insurer pays you a declared interest rate (e.g., 3%).

- No call options are purchased for this portion.

So:

- $20,000 → Bonds → Declared rate credited (e.g., 3%).

2) Index Account Portion – $80,000

This part is trickier, because it’s linked to S&P 500® index credits. The mechanics:

- The insurer invests the principal ($80,000) safely in bonds (not stocks).

- Let’s assume current bond yield ≈ 5%. That produces:

- $80,000 × 5% = $4,000 annual yield.

- From that $4,000, the insurer:

- Keeps some for expenses & profit margin (say 0.5% of principal, or $400).

- The remaining $3,600 is the options budget.

- With $3,600, the insurer buys call options on S&P 500®.

- If S&P goes up, the options generate a payout, which is credited to the policy (up to cap/participation).

- If S&P goes down, the options expire worthless (loss of option budget, counting onto the insurer)→ credit to the policy = 0%.

3) Putting it together

- $20,000 Fixed Account: Bonds only → declared rate credited directly.

- $80,000 Index Account:

- Bonds hold the $80,000 safe.

- ~$3,600 options budget (from bond yield net of margin) funds call options.

- Options outcome determines index credit (subject to cap/participation).

✅ Simplified Illustration (assume 5% bond yield, 0.5% margin, see Figure 2 below)

- Fixed Account: $20,000 → earns declared 3% = $600 credited.

- Index Account:

- $80,000 bonds safe.

- $4,000 bond yield – $400 margin = $3,600 option budget.

- $3,600 buys S&P 500® call options.

- Index goes up → payout credited to the policy (up to cap/participation).

- Index flat/down → loss of option budget counting onto the issuer; no credit to the policy (0% floor).

Figure 2: Illustration of two accounts in IUL.

Leave a comment