Roth accounts are among the most powerful tools in U.S. retirement planning because they create tax-free income in retirement, which provides flexibility, tax diversification, and protection from future tax increases. Below is a deep but structured analysis of Roth IRA and Roth 401(k) from a financial planning perspective.

1. Core Concept of Roth Accounts

Both Roth IRA and Roth 401(k) operate on the same fundamental tax principle:

You pay taxes now, but withdrawals later are tax-free.

This contrasts with traditional retirement accounts:

| Account Type | Tax Now | Tax Later |

| Traditional IRA / 401(k) | Deductible now | Taxed in retirement |

| Roth IRA / Roth 401(k) | No deduction now | Tax-free later |

If rules are satisfied (age 59½ and account open ≥5 years), withdrawals of both principal and earnings are completely tax-free.

This tax structure creates enormous long-term planning advantages.

2. Roth IRA – Deep Analysis

Definition

A Roth IRA is an individual retirement account funded with after-tax contributions, allowing tax-free growth and withdrawals.

Key advantages make it one of the most flexible retirement vehicles.

Roth IRA Contribution Rules (2026 approximate)

Contribution limits are set annually by the Internal Revenue Service.

Typical limits (recent range):

| Age | Annual Contribution |

| Under 50 | $7,000 |

| 50+ | $8,000 (catch-up) |

Income Limits

Roth IRA eligibility phases out for higher incomes.

Example approximate ranges:

| Filing Status | Phase-out Range |

| Single | ~$146k – $161k |

| Married Filing Jointly | ~$230k – $240k |

High earners often use Backdoor Roth strategies.

Major Roth IRA Advantages

1. Tax-Free Retirement Income

Once qualified:

- contributions → tax-free

- growth → tax-free

- withdrawals → tax-free

This creates true tax-free income streams.

Example:

Investment grows:

$7,000/year × 30 years

7% return

Future value ≈ $660,000+

Traditional IRA: taxable

Roth IRA: 0% tax

2. No Required Minimum Distributions (RMD)

Traditional retirement accounts must start withdrawals at age 73 (per the SECURE 2.0 Act).

Roth IRA:

No RMD during the owner’s lifetime.

Benefits:

• money keeps compounding

• tax-free inheritance planning

• flexible retirement timing

3. Contribution Liquidity

Roth IRA contributions can be withdrawn any time tax-free and penalty-free.

Order of withdrawals:

- Contributions

- Conversions

- Earnings

This provides emergency flexibility.

4. Estate Planning Advantage

Beneficiaries receive:

tax-free distributions

Although inherited Roth IRAs now must typically follow a 10-year withdrawal rule, the growth remains tax-free.

5. First-Home Withdrawal

Roth IRA allows:

$10,000 tax-free withdrawal for first-time home purchase.

3. Roth 401(k) – Deep Analysis

A Roth 401(k) is an employer-sponsored retirement account that allows after-tax contributions inside a 401(k) plan.

It combines the high contribution limits of 401(k) with Roth tax treatment.

Contribution Limits (2026 approximate)

| Age | Annual Limit |

| Under 50 | ~$23,500 |

| 50+ | ~$31,000 |

This is much higher than Roth IRA.

Important:

The limit applies combined across traditional + Roth 401(k).

Employer Matching

Employers often match contributions.

Important rule:

Employer match goes into traditional (pre-tax) side.

Example:

Employee contributes:

$20,000 Roth 401(k)

Employer match:

$6,000 → traditional 401(k)

Result:

Two tax buckets inside the plan.

Required Minimum Distributions

Historically Roth 401(k) had RMD.

However, starting in 2024, the SECURE 2.0 Act eliminated RMD for Roth 401(k) accounts.

This aligned Roth 401(k) with Roth IRA.

Roth 401(k) Advantages

1. Much Higher Contribution Limit

Roth IRA: ~$7k

Roth 401(k): ~$23k+

High earners can build large tax-free pools.

2. Automatic Payroll Investing

Behavioral finance advantage:

- automatic deductions

- disciplined savings

- employer match

3. No Income Limits

Unlike Roth IRA:

Anyone can contribute to Roth 401(k) regardless of income.

High-income professionals often rely on this.

4. Mega Backdoor Roth Opportunity

Some plans allow:

After-tax contributions up to ~$69k total plan limit.

Then convert to Roth.

This is called Mega Backdoor Roth.

It can create six-figure annual Roth contributions.

4. Roth vs Traditional Strategy (Tax Diversification)

A key retirement planning principle is tax diversification.

Sources of retirement income may include:

| Tax Category | Examples |

| Taxable | brokerage accounts |

| Tax-deferred | Traditional IRA / 401(k) |

| Tax-free | Roth IRA / Roth 401(k) |

This allows retirees to control their taxable income each year.

Example strategy:

Withdraw from:

- Traditional accounts to fill low tax brackets

- Roth accounts to avoid higher brackets

This can reduce:

- Medicare IRMAA surcharges

- Social Security taxation

- overall lifetime taxes

5. Why Roth Accounts Are Powerful for Retirement Planning

1. Protection Against Future Tax Increases

The U.S. national debt exceeds $34 trillion.

Many economists expect higher tax rates in the future.

Roth accounts lock in today’s tax rates.

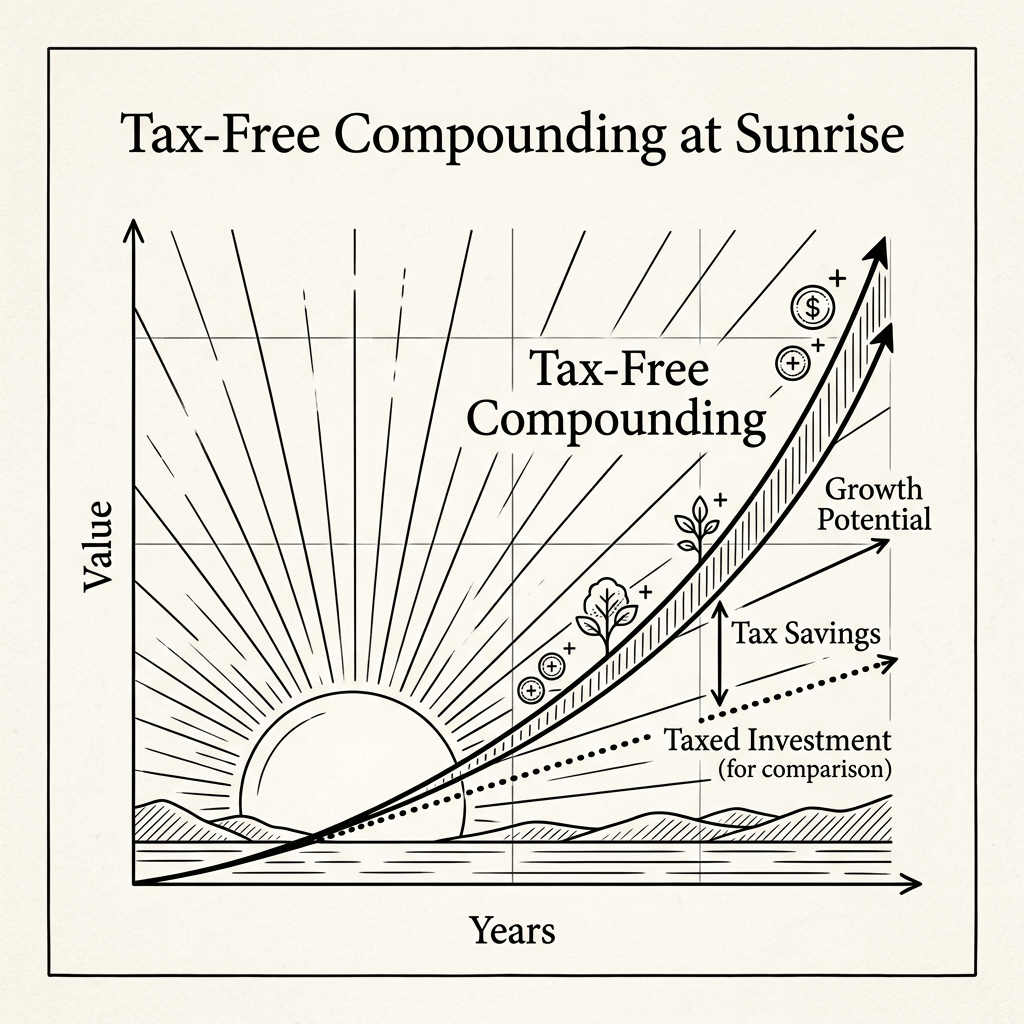

2. Tax-Free Compounding

Compounding without tax drag creates enormous differences over decades.

Example:

$10k/year × 30 years

7% return

Future value ≈ $1M+

Traditional: taxable

Roth: fully tax-free

3. Flexible Retirement Income

Roth withdrawals:

• do not increase taxable income

• do not affect Social Security taxation

• do not increase Medicare premiums

This makes them excellent income-smoothing tools.

4. Estate Planning Efficiency

Roth assets:

• pass to heirs tax-free

• continue growing tax-free during 10-year rule period

This creates a tax-efficient legacy asset.

6. Typical Roth Strategy in Professional Planning

Many financial planners recommend a three-bucket strategy:

During working years

1️⃣ Max employer match in 401(k)

2️⃣ Max Roth IRA

3️⃣ Contribute to Roth 401(k) or Traditional 401(k) depending on tax bracket

4️⃣ Use Backdoor Roth if income too high

Pre-retirement (age 55–70)

Use Roth conversions to manage tax brackets.

Retirement

Withdraw:

1️⃣ taxable accounts first

2️⃣ traditional accounts strategically

3️⃣ Roth accounts last

7. Simple Summary

| Feature | Roth IRA | Roth 401(k) |

| Tax treatment | After-tax | After-tax |

| Growth | Tax-free | Tax-free |

| Withdrawals | Tax-free | Tax-free |

| Contribution limit | Low | High |

| Income limits | Yes | No |

| RMD | None | None (after 2024) |

| Employer match | No | Yes |

✅ Core Value

Roth accounts create:

tax-free retirement income + tax diversification + estate efficiency

That combination makes them one of the most powerful long-term financial planning tools available in the U.S. retirement system.

Leave a comment